The Maqasid al- Shariah in

Management Strategy of Islamic Bank

by SHAYA’A OTHMAN

INTRODUCTION

The business of banking in Malaysia came into force with the introduction of the Central Bank of Malaya Ordinance, 1958 (CBO), and on 26 January 1959 the Central Bank of Malaysia or known in Malay as Bank Negara Malaysia (BNM), was first being established in the then Federation of Malaya. This ordinance was further revised in 1994 and renamed as the Central Bank of Malaysia Act 1958 (revised -1994). Under this Act, the roles of Bank Negara Malaysia are defined, which constitutes the apex of the monetary and banking structure of Malaysia, with the objectives to include the following:

- Issue currency and keep the reserves safeguarding the value of currenc.

- Act as a banker and financial adviser to the Government.

- Promote monetary stability and a sound financial structure; and

- Influence the credit situation to the advantage of Malaysia.

The introduction of Islamic Bank in Malaysia was driven by the growing interest of number of Muslims who want to lead their way of lives in accordance with Shariah which include the area of banking and finance. In response to this development Government of Malaysia enacted a separated banking legislation, the Islamic Bank Act 1983. This enactment enables the establishment of Islamic banking to run side-by-side with conventional banking. Later in the same year the Government Investment Act 1983 was also being enacted, to allow the Government to issues Government Investment Issues based on Islamic principles. The Act also enables Islamic banks to meet their liquidity requirements as well as acting as an instruments to absorb idle funds in the short run. The same with all other conventional banks, Bank Negara Malaysia was given absolute powers under the provision of Islamic Bank Act 1983, to regulate and supervise the Islamic banks licensed under this Act

DEVELOPMENT OF ISLAMIC BANK

The first known Islamic bank was first introduced in 1963 in Egypt at Mit Ghamr by Ahmad El Najjar. Unlike conventional this bank based on sharia, whereby no interest was charged to investors and borrowers. Unfortunately this bank lasted for less than 5 years. It stopped operation in 1967.

Another interesting development in 1963 was the establishing of an Islamic institution in Malaysia known as the Tabong Haji Malaysia was established in 1963. I share the view of Khir, Gupta and Shanmugam (2008), that “Islamic banking, with a very different approach to that in Egypt, also emerged in Malaysia. It was a financial institution developed for Malaysia Muslims undertaken the pilgrimage to Mecca and medina. This institution called Lembaga Tabung Haji (Pilgrims Fund Board, Malaysia) was set up to help Muslims save for their pilgrimage expanses’.

In 1971, another bank known as Nasser Social Bank was later established in Egypt. Although it makes no reference to sharia, but it declared as an interest-free commercial bank, and it may be considered as Islamic bank. The development of Islamic banking also taken place in Philippine, which is a prominently Christian Catholic nation. Bank Amanah was established here in 1973, and has survived without any state intervention.

The establishment of Islamic Development Bank [IDB} in 1975 by the Organisation of Islamic Countries (OIC), marked the mile stone the significant development of Islamic bank, and triggered the formation of Islamic banks all over the world, not only in the Muslims countries but also in the Christendom, especially in the European Unions. The formation of IDB by the OIC members resembles to that of World Bank and Asian Development Bank (ADB).

In Malaysia, although Lembaga Tabung Haji was established in 1963, the first full-flashed Islamic commercial bank was established in July 1983, known as Bank Islam Malaysia Berhad (BIMB). It was established, when the Islamic Banking Act 1983 was enacted by Malaysian Government, and BIMB is the first commercial Islamic Bank licensed under this Act. The introduction of Islamic Banking Scheme Skim Perbankan Islam –SPI) 1998, by Bank Negara Malaysia, further allowing conventional banks to offer Islamic banking products and services which are in compliance with Shariah.

The development of Islamic bank is not confined to Islamic countries only but also to other countries such as the United States of America, European Union, Australia, Singapore, Thailand and Hongkong. Interestingly, non-Muslims countries like United Kingdom, Singapore and Hongkong are trying to develop centres as hub for Islamic products and services. Figure 1 shows the development of Islamic Banking.

Figure1. Establishment of Islamic Banks (1960- 2002)

PURPOSE OF ESTABLISHING ISLAMIC BANK

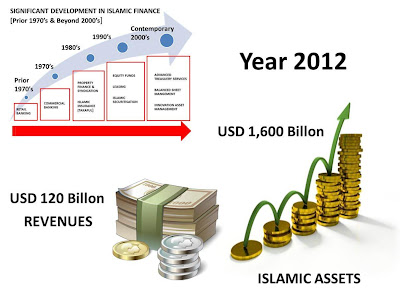

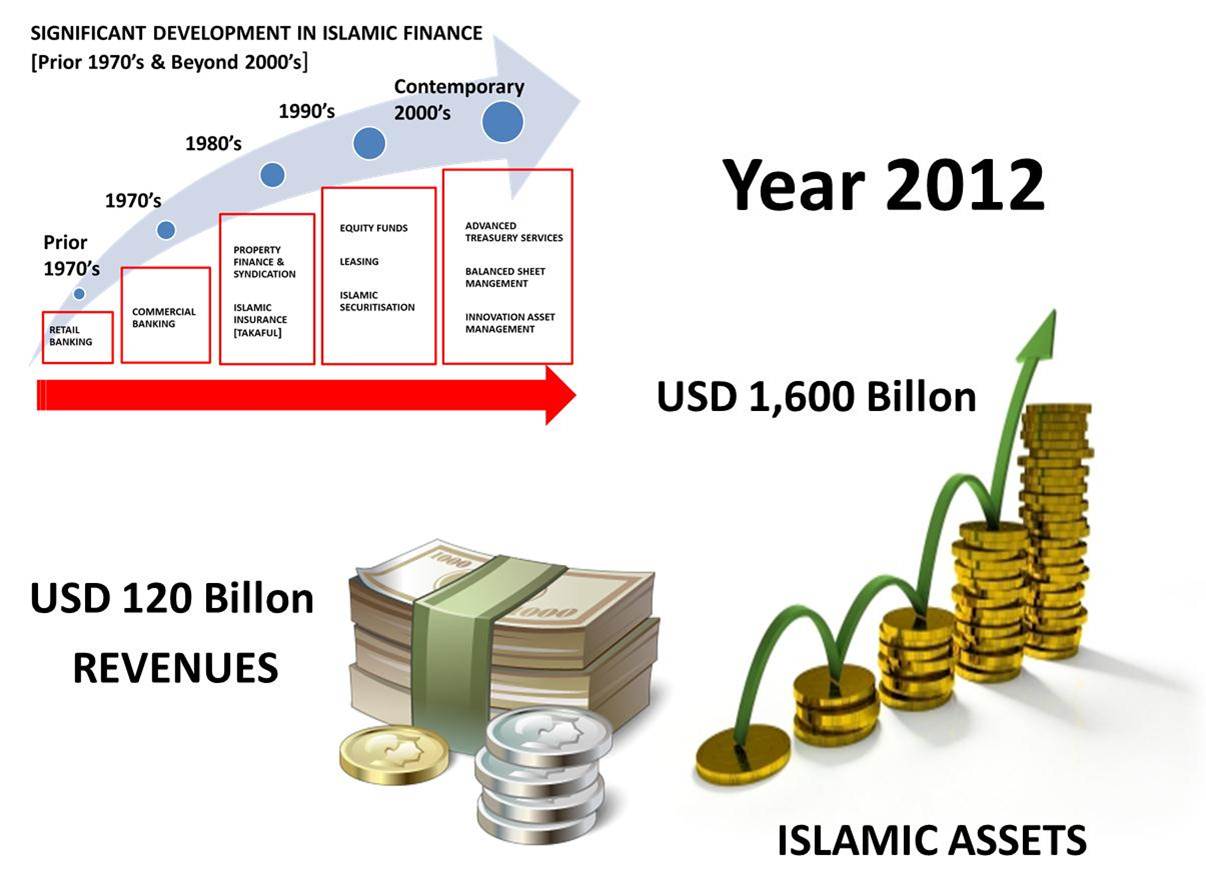

It is observed that the early establishment of Islamic bank was meant to provide services to Muslims who want to practice Shariah in their way of life which were relating to financial activities, as the case of establishing Mit Ghamar Local Islamic Bank (1963) in Egypt. The products or services provide by the Islamic bank develop from retail banking only prior in 1970s, to fully commercial banking in 1970s, and develop further to property finance and syndication in 1980s. In 1990s the services provide by Islamic Bank include more to equity funds and Islamic securitization, and today it developed actively in areas of treasury services, balance management and innovation asset management. Figure 2 shows this significant development.

Figure2: Significant Development of Islamic Finance 1970s

Khir,et al (2008), explained that Islamic banks are financial intuitions established to promote Islamic economics. An Islamic economy is a market economy guided by moral values. Islam differs essentially from capitalism and socialism in nature of ownership. Islam has given detailed regulations for economic life, which is balanced and fair. According to the Holy Quran, everything on this earth belongs to Allah the Almighty. Man is mere trusty and he is accountable to Allah in accordance with the rules laid down in the Sharia. The fundamental principles of an Islamic Economy system include the following;

1. Socio-Economic Justice and Equitable Distributions

2. Trading of forbidden objects

3. Trusteeship

4. Prohibition of Hoarding

5. Spirit of Corporation

6. Duality of Risk

7. No gain without either effort or liability

.

Karim (2005), elaborate further on Sharia whereby Sharia is an Arabic word that literally means “the road to take or the line to follow.” Sheikh Syalthut (1959) p.68, defines further the terminology of Sharia as a set of divinely pre-sanctioned lost and rulings, or prescribed principles which Muslim should abide themselves so they can relate to Allah as well as other human beings

Muslim scholars are of the opinion that the ultimate objectives [maqasid al-Sariah] which are a necessity [al-daruriyyah] for mankind to be able to live peacefully in this world, according to al-Quran and al-Sunnah, include five main areas – [1] Protection of life, [2] Protection of al-Din [Islam], [3] Protection of Progeny or Offspring, [4] Protection of Intellect or Faculty of Reason, and, lastly, [5] Protection of Material Wealth or Resources. From a review of the related literature, little is mentioned or discussed about Islamic banks working towards achieving these ultimate objectives or maqasid al-Shariah.

Here we are not going to discuss the order of importance or priority to these five objectives of shariah, or Maqasid al-shariah. But I share the view of Gamal Eldin Attia (2010) that we have to acknowledge the arrangement posed by al-Ghazali *(505 HA/1111 AC), which became most widely acceptable thereafter, notably in the following order of priority:

1. Protection of al-Din (Islam)

2. Protection of Life

3. Protection of Intellect or Faculty of Reason

4. Protection of Progeny or Offspring

5. Protection of Material Wealth.

MAQASID AL-SHARIAH IN ISLAMIC BANKING

It is observed as to date there is not much discussion on the application of Maqasid al-Syariah [Ultimate objectives of Syariah] in the formulation of Strategic Planning in Islamic banks. The management of Islamic financial institutions such as Islamic banks and Islamic insurance companies should look beyond profit. Although profit is very important for the institution to be able to exist, it is not the main objective of the institution. Profit is just like oxygen in our bodies which is essential for us to stay alive, but which is not the main objective.

Today non-Muslims are getting inroad into the business of Islamic banking, even the name of the bank is confusing to the public. For Example Hong Leong Islamic Bank of Malaysia, is totally owned by non-Muslim. The name “Hong Leong” itself reflects that the bank is owned by non–Muslim but Islamic. Could be in the future that more non-Muslim names reflected as the name of Islamic Bank owned by non-Muslims? The question is whether the current Islamic banks owned by non-Muslims will be able to incorporate Maqasid al-Shariah into their management strategies so as to justify being “Islamic”.

What are the objectives of the many conventional banks which are rushing to “convert” their products but not themselves into “Islamic Banks” or provide open windows of “Islamic Banks”? Are they attracted to the ultimate objectives [Maqasid al-Shariah] as advocated by Islam? Or are they attracted to make profits from the abundant wealth of Muslims?

Also, is there is any rationale whatsoever for countries predominantly populated by non–Muslims and governed by non-Muslims becoming Islamic Financial Centres? London, Singapore and Hong Kong are all planning to establish such centres, and the question arises as to whether maqasid al-Syariah is being incorporated into their blueprints for creating these centres?

FUTURE SUSTAINABILITY OF ISLAMIC BANK

In year 2012 the asset management under the management of Islamic Instructions is estimated to be around USD1,600 billion and revenues to be around USD120 billion. The future growths and sustainability of Islamic finance could be realized if Maqasid a-Syariah is put in place in all Islamic Banks. If not Islamic Banks will experience the disastrous financial melting down as experienced recently by conventional banks.

Curtis, G. (2008) in his research of the main causes of the recent financial meltdown, concludes that “the root cause of the crisis was the gradual but ultimately complete collapse of ethical behaviour across the financial industry. Once the financial industry came unmoored from its ethical base, financial firms were free to behave in ways that were in their – and especially their top executives’ – short-term interest without any concern about the longer term impact on the industry’s customers, on the broader American economy, or even on the firms’ own employees”. This conclusion may be capsulized in other words of “the non-compliance to Maqasid al-Shariah”, particularly in the area of “Islamic Ethic”.

It is proposed that Maqasid Al-Shariah need to be incorporated in the present management strategy of all Islamic banks. Though profitability is essential and must be achieved, but it is not the main objective. In Islam, the ultimate objectives of any activities including business activities are ultimately with the aim of achieving objectives of Shariah or Maqasid al-Shariah.

CONCLUSION

Strictly, I have the view that the current practice of Islamic banks needs to incorporate Maqasid al-Shariah into their management strategy to ensure its sustainability to serve mankind in the future, in confirmation to the requirement of Shariah. Otherwise, the use of the word ‘Islamic’ should be dropped. Furthermore, it is proposed that the term ‘Islamic Bank’ should be reviewed, and should only be used to refer to an ‘Islamic Bank’ owned and managed by Muslims. This is because Muslims are the only community [ummah] recognised by Allah, that can or able to uphold Maqasid al-Shariah. Islamic banks owned by non-Muslims may be called ‘Interest Free Banks’.

References:

Gamal Eldin Attia ( 2010). Towards Realization of The higher Intents of Islamic law : Maqasid al-Shariah a functional Approach. Kuala Lumpur. Islamic Book Trust.

Khir, K. Gupta, L. Shanmugam, B (2008). Islamic Banking: A Practical Perspective, Selangor, Malaysia. Pearson-Longman

Curtis, G. (2008). White Paper No. 44 – The Financial Crisis and the Collapse of Ethical Behavior , Greycourt & Co., Inc.

Beekun, R. I.,(2006). Strategic Planning and Implementation for Islamic Organizations. London. International Institute of Islamic Thought.

Karim, A. A., (2005). Islamic Banking: Fiqh and Financial Analysis, Jakarta, PT Radjagrafindoprasada.

The Central and The Financial System in Malaysia: A Decade of Changes (1999) Bank Negara Malaysia, Kuala Lumpur

The Central Bank and the financial System in Malaysia: A decade of Change 1989-1999 (1999). Kuala Lumpur. Bank Negara Malaysia

{kind=link}