Application of

Maqasid Al Shariah in Business Strategy

By

Dr Shaya'a Othman

Please click the above image or the link below to see and download the whole slide

https://designrr.page/?id=444106&token=2807225661&type=FP&h=4490

Application of

Maqasid Al Shariah in Business Strategy

By

Dr Shaya'a Othman

https://designrr.page/?id=444106&token=2807225661&type=FP&h=4490

Transforming

Conventional Hotel Operational Business Hotel to a Shariah Hotel

By

Dr SHAYA'A OTHMAN

Please click the above slide or the link below to read the complete Slides and to download

https://designrr.page/?id=443519&token=234094679&type=FP&h=2032&singlePage=1&startPage=10

مقدمة المترجم والمراجع

نشهد اليوم عصرًا يشهد تسارعًا مذهلاً في التقدم التكنولوجي، حيث تغزو الابتكارات والتحولات الرقمية حياتنا اليومية بوتيرة أسرع من قدرتنا على استيعابها، مما يطرح تحديات جديدة وفرصًا واعدة، وفي ظل هذا التطور المتسارع، يواجه قطاع التعليم تحديات كبيرة في مواكبة أحدث المناهج والأساليب التقنية؛ ومع ذلك، فإن التحولات الرقمية تحمل في طياتها فرصًا عظيمة لتطوير العملية التعليمية وتوسيع آفاق المعرفة، فيتعيّن علينا لاستغلال هذه الفرص بشكل أمثل، أن نعتمد على منهجية واضحة ملتزمة بمبادئ وضوابط الشريعة الإسلامية.

إن الشريعة الإسلامية، بحكم كونها شاملة لكل مناحي الحياة، تقدم الإطار الأخلاقي والقيمي الذي يجب أن يٌبنى عليه كل مجال، ومنها التعليم، فهي تشجع التطور العلمي والمعرفي، وتوجهه نحو تحقيق الخير للفرد والمجتمع، فالعلم يوسع مدارك الإنسان ويزيد إيمانه بربه، كما أنه يساعد على فهم الكون وقوانينه قال الله تعال: "يَرْفَعِ اللَّهُ الَّذِينَ آمَنُوا مِنْكُمْ وَالَّذِينَ أُوتُوا الْعِلْمَ دَرَجَاتٍ."(سورة المجادلة، الآية، 11)، هذه الآية تربط بين الإيمان والعلم، وتشير إلى أن العلم يرفع درجة الإنسان، فيمكننا بسهولة دمج المناهج العالمية الحديثة في التعليم الشرعي، حيث تركز على قياس الثمرات التعليمية وتراعي الفروق الفردية؛ بحيث يمكن أن تسهم بشكل كبير في تطوير العملية التعليمية مدعوما باستغلال العالم الرقمي في عرض البرامج والمناهج بشكل تفاعلي، والوصول إلى كل طالب علم، وهذا لا يتأتى إلا بالحفاظ على القيم والأخلاق الإسلامية، فيمكننا بناء نظام تعليمي متكامل يجمع بين المعرفة العلمية والأخلاق الفاضلة، مما يخرج أجيالاً قادرة على مواجهة تحديات العصر والحفاظ على هويتها الإسلامية.

ممّا سبق يُولد لنا هذا الكتاب الذي بين أيدينا للدكتور شعياء عثمان المؤلّف لـ: سلسلة كتب لدمج مقاصد الشريعة الإسلامية في تنمية الأمة اقتصاديا، اجتماعيا، علميا، ثقافيا، وإداريّا، فيمثل عمل الدكتور شعياء عثمان نقلة نوعية في مجال التعليم السيبراني، حيث قدم إسهامًا مبتكرًا بتوسيع نطاق مفهوم السيبرانية ليشمل التعليم بشكل عام، متجاوزًا بذلك التركيز التقليدي على الأمن السيبراني. وقد تجلى ذلك في اختياره لعنوان الكتاب " مقاصد الشريعة استراتيجية للتعليم السيبراني الإسلامي"، الذي يوضح هدفه في ربط التعليم السيبراني بالتعاليم الإسلامية ومقاصد الشريعة، أي: تقديم استراتيجية مبنية على مقاصد الشريعة لتطبيقها في مجال التعليم السيبراني. وذلك بابتكاره نموذج جديد يستند إلى مفهوم سلسلة القيمة لبورتر، ليتم تطبيقه على البيئة التعليمية الرقمية، مع ضمان دمج القيم الإسلامية في كل مرحلة من مراحل العملية التعليمية، بدءًا من تصميم المناهج وصولاً إلى الخدمات المقدمة للطلاب وتطوير البنية التحتية الرقمية، كما لم يفوّت المؤلف الفرصة ليضع بين أيدينا، رؤية مستقبلية للتعليم الإسلامي من خلال اقتراح نموذجين مبتكرين هما المركز الدولي للتعليم السيبراني الإسلامي (IICEC) والجامعة السيبرانية الإسلامية الدولية (IICU)، بهدف تحقيق نقلة نوعية في التعليم الإسلامي عبر توفير منصات تعليمية متقدمة ومرنة، تصل إلى شرائح واسعة من المتعلمين في مختلف أنحاء العالم، فمن خلال IICEC، يمكن للمتعلمين الوصول إلى مجموعة واسعة من البرامج التعليمية من مختلف الجامعات الشريكة، بينما تقدم IICU تجربة جامعية كاملة عن بعد، تضمن جودة تعليمية عالية مع الحفاظ على القيم الإسلامية، مذيّلا هذان المقترحان بالإجراءات العملية اللازمة لإنشاء النموذجين على أرض الواقع.

ختاما، فإنّ هدفنا الأسمى هو بناء مجتمع صالح يرضى الله ورسوله، وللوصول إلى هذا الهدف، يجب علينا أن نستفيد من تجارب الأمم الأخرى، مع الحرص على تكييفها وفقًا لمبادئنا الإسلامية، فبهذه الطريقة يمكننا تحقيق التقدم والازدهار في الدنيا والآخرة.

وإنّي لأسأل الله تعالى التوفيق والسداد في اختياري للمصطلحات والترجمة دون أن أنقص من جوهر وفكرة الكتاب.

والله الموفق،

ترجمة وراجعة: د. الطيب مبروكي

وكيل الجامعة للشؤون الأكاديمية- السابق-

جامعة المدينة العالمية – ماليزيا-

يم الكتاب

في ظل التحول الرقمي المتسارع في التعليم، يواجهنا تحدي الحفاظ على القيم الأخلاقية، وللاستفادة من هذا التقدم الرقمي يقدم هذا الكتاب حلًا مبتكرًا من خلال تقديم نموذج للتعليم السيبراني المستند إلى مبادئ الشريعة الإسلامية، ليوازن بين متطلبات العصر واحتياجاتنا الروحية، كما يقدّم المؤلف إطارًا عمليًا لمواءمة التقنيات الحديثة مع القيم الإسلامية، ليصنع جيلًا متعلمًا وواعٍ بقيمه.

يقدم هذا العمل إطارًا مبتكرًا لتطبيق نموذج سلسلة القيمة على التعليم السيبراني لـ شعياء عثمان (2024)، مستلهماً مقاصد الشريعة الإسلامية، من خلال نموذج بورتر لسلسلة القيمة على البيئة التعليمية الرقمية، مع ضمان انعكاس القيم الإسلامية على جميع جوانب العملية التعليمية السيبرانية من خدمة الطلاب وتصميم المناهج وتطوير المنظومة التقنية، ويحرص المؤلف هنا على التطبيق الدقيق للنموذج والذي سيؤدي إلى تطوير نظام تعليمي متكامل يراعي الجوانب الأخلاقية والاجتماعية والتنموية للفرد والمجتمع، كما يوفر هذا النموذج خارطة طريق للمؤسسات التعليمية لتصميم وتنفيذ برامج تعليمية تعزز التنمية الشاملة للفرد والمجتمع.

يقترح الكتاب نموذجين مبتكرين هما المركز الدولي للتعليم السيبراني الإسلامي (IICEC) والجامعة السيبرانية الإسلامية الدولية (IICU) لتوسيع نطاق التعليم الإسلامي عالميًا. بحيث يهدف هذان النموذجان إلى تحقيق نقلة نوعية في التعليم الإسلامي، من خلال توفير فرص تعليمية متاحة للجميع وعالية الجودة، وتلبية احتياجات المتعلمين في مختلف أنحاء العالم، وذلك بعقد بحيث، يوفر IICEC منصة شاملة للوصول إلى برامج تعليمية متميزة لتبادل الخبرات من مختلف الجامعات الشريكة، بينما تقدم IICU تجربة تعليمية جامعية كاملة عن بعد، مما يضمن جودة تعليمية عالية مع الحفاظ على القيم الإسلامية.

يمثل هذا الكتاب دليلًا ومرجعًا شاملاً للمعلمين والإداريين وصناع السياسات الراغبين في دمج التكنولوجيا في التعليم الإسلامي بطريقة تتوافق مع القيم الأخلاقية. إنه عمل رائد يفتح آفاقًا جديدة في مجال التعليم الرقمي الإسلامي.

قدّمه:

الأستاذ الفخري داتو ويرا الدكتور جميل عثمان

مستشار،

المعهد الدولي للفكر الإسلامي (IIIT) الولايات المتحدة الأمريكية،

المركز الإقليمي لشرق وجنوب شرق آسيا، ماليزيا

الجامعة الإسلامية العالمية ماليزيا 08, [IIUM] نوفمبر 2024

OVERRIDING STRATEGY

IN DEVELOPING THE CAMBODIAN MUSLIM COMMUNITY

By

DR SHAYA'A bin OTHMAN

You can buy this Book for USD 2.00 by clicking the following

NOTE

" This book was first published and officially launched during the opening ceremony of the University of Cambodia University of Management and Technology (CUMT), marking an important milestone in the Cambodian Muslim community’s contribution to the development of higher education. The University is not only for Cambodian Muslims but also for all Cambodians, reflecting our broader commitment to national progress.

A special acknowledgement goes to Dr. Shaya’a bin Othman for his efforts in writing this book, *Overriding Strategy in Developing the Cambodian Community*, which outlines strategies for the Cambodian Muslim community to organize and chart their contributions. He proposes tactical approaches in the fields of education, social development, and economic growth, including the formulation of an Islamic Quality Standard—an integrated educational syllabus that combines Islamic revealed knowledge with conventional technical knowledge for all schools, colleges, and universities. Additionally, he emphasizes the need to establish educational infrastructures, whether hybrid or online, including schools, colleges, and universities, to further these goals.

This book, also suggests the establishment of the Cambodian Muslim Wakaf Development Foundation (CMWD), which would not only focus on education but also on the social and economic development of the Muslim community. He advocates for CMWD to adopt *Maqasid alShariah* (The Developmental Ultimate Objectives of Shariah) as an overarching strategy, ensuring that efforts in education, social development, and economic growth are aligned and mutually reinforcing."

His Excellency Dr Husen Mohammad Farid

President of the Board of Trustees Cambodia University of Management and Technology 21st October 2024

FORWARD

" A clear strategy is essential for managing an organization or developing society, as it provides direction, prioritizes resources, and aligns efforts toward common goals. A well-defined strategy helps navigate challenges, adapt to changes, and ensure sustainable growth. It fosters coordinated action, accountability, and long-term success by guiding decision-making and optimizing overall performance. Many strategies are well-known in both the private and public sectors, notably Michael Porter's *Competitive Strategy* (1980) and Kim and Mauborgne’s *Blue Ocean Strategy* (2005), both from Harvard University. These strategies focus on achieving profitability and sustaining growth. Some governments have attempted to adopt these strategies in their development plans. *Maqasid Al-Shariah* (MAS) has been widely discussed and developed in the field of Islamic law and judiciary, but its application in management and development has been explored far less.

In the context of societal development, Muslim scholars and professionals have sought an Islamic management model that serves as a practical guide. The application of MAS as a development strategy addresses the economic, social, and institutional changes necessary for building sustainable societies. While many countries engage 6 in strategic planning, they often lack a system to effectively coordinate these processes for the development of the Muslim community.

MAS can create a coordination system that integrates all aspects of sustainable development into mainstream planning. Improved coordination across different frameworks can also ease capacity challenges and resource constraints. This book explores how the five MAS principles—Protection of Religion, Protection of Life, Protection of Intellect, Protection of Offspring, and Protection of Wealth—can be embedded as key strategies for the development of the Cambodian Muslim minority community. The proposed implementation structure, through the Cambodian Muslim Wakaf Development Foundation (CMWD), ensures that the community can develop independently and sustainably in education, social development, and economics. This approach will create job opportunities and promote entrepreneurship in fields overseen by CMWD.

Prof Emeritus Dato’ Dr Wira Jamil Osman

Advisor, Cambodia University of Management and Technology

21st October 2024

FORWARD

The rapid digitalization of education is reshaping the educational landscape, presenting unique opportunities and challenges. This book enters the field with an innovative and much-needed approach, pioneering the concept of Cyber Education grounded in the principles of Maqasid al-Shariah—the higher objectives of Islamic law. By aligning cyber education practices with Islamic values, the author not only preserves the integrity of Islamic ethics but also extends them into the virtual sphere, thus presenting a model that is simultaneously modern and rooted in tradition.

Central to this work is the Shayaa Othman Cyber Education Value Chain Strategy Model (2024), a framework that thoughtfully applies Porter’s Value Chain to the digital educational environment, with Maqasid al-Shariah as the guiding strategy. This approach ensures that each aspect of educational delivery—from course design and technology development to student support—is imbued with values prioritising ethical responsibility, holistic development, and social welfare. The author’s application of this model is both academically rigorous and highly practical, offering a pathway for institutions to implement a value-driven education system that resonates deeply with Islamic ideals.

In proposing both the International Islamic Cyber Education Center (IICEC) and the International Islamic Cyber University (IICU) models, the book provides a versatile blueprint for institutions looking to expand Islamic education globally without compromising on quality or values. The IICEC model serves as an accessible, scalable hub for Islamic education, connecting students with reputable programs from partner universities worldwide. The IICU model, on the other hand, envisions a fully accredited online university, promising a transformative role in delivering comprehensive Islamic education.

This book is an essential resource for educators, administrators, and policymakers aspiring to harness the potential of technology in education while upholding Islamic ethics. It is with great pleasure and anticipation that I commend this groundbreaking work, which I believe will serve as a beacon for Islamic education in the digital age.

Prof Emeritus Dato’ Wira Dr Jamil Osman

Advisor, International Institute of Islamic Thought (IIIT) USA, East & South East Asia Regional Center, Malaysia, International Islamic University Malaysia [IIUM], 8th November 2024

PREFACE

The rapid

transformation of technology has reshaped education globally, creating new

opportunities to deliver accessible, flexible, and high-quality learning

experiences. Among these innovations, Cyber Education stands out as a

progressive model, distinct from traditional online learning. This book

presents a comprehensive exploration of Cyber Education within an Islamic

framework, integrating the principles of Maqasid al-Shariah—the ultimate

objectives of Islamic law. By weaving these principles into Cyber Education, we

envision an educational model that is ethically driven, globally accessible,

and responsive to the needs of modern learners.

In Chapter

1, the discussion begins with the evolution of Cyber Learning and

how it extends beyond conventional online education. Unlike traditional

formats, Cyber Education encompasses a holistic digital ecosystem where

emerging technologies such as virtual reality, artificial intelligence, and

secure digital infrastructures enrich the learning experience. By grounding

Cyber Learning in the concept of Maqasid al-Shariah, we introduce a

value-driven approach that maintains Islamic ethical standards while embracing

the technological advances that define 21st-century education.

Chapter 2 presents a

detailed analysis of online university development in Malaysia, highlighting

the country's unique advancements and challenges in digital education. While

Malaysia’s online education sector is still growing, institutions like Open

University Malaysia and Asia e University have made significant strides in

providing flexible learning options that serve diverse populations. The

insights gathered from Malaysia’s approach inform later discussions on

developing similar institutions in an Islamic context.

In Chapter

3, we examine the influence of secularism in education, especially its

tendency to separate knowledge from moral and spiritual dimensions. By

contrasting secular educational frameworks with Islamic principles, this

chapter underscores the value of a Maqasid al-Shariah approach in maintaining a

balanced, purpose-driven educational environment that nurtures both

intellectual and ethical development.

Chapters 4 and 5 focus on

integrating Maqasid al-Shariah into strategic management for Cyber

Education. Chapter 4 explores how the five primary objectives of

Shariah—protection of religion, life, intellect, offspring, and wealth—can

serve as an overarching strategy, guiding all educational activities. Chapter 5

builds on this by presenting David’s Strategic Management Framework

integrated with Maqasid al-Shariah, offering a model that aligns organizational

goals with Islamic values and ethical responsibilities.

The Shayaa

Othman Cyber Education Value Chain Strategy Model (2024), introduced in Chapter

6, adapts Porter’s Value Chain for Cyber Education, with Maqasid al-Shariah

as the foundational strategy. This model divides educational activities into

primary and support functions, each designed to enhance the learning experience

while upholding Islamic values. Support activities, such as technology

development and human resources, provide essential infrastructure, while

primary activities like content creation, course delivery, and student support

services focus on the core mission of Cyber Education.

The book’s

final two chapters propose practical frameworks for establishing Islamic Cyber

Education institutions. Chapter 7 details the International Islamic

Cyber Education Center (IICEC) Model, a concept inspired by platforms like

Amazon and Coursera, which would serve as an aggregator connecting students

with partner universities worldwide. Through partnerships with reputable

Islamic institutions, IIICEC could offer students access to a wide range of

accredited programs, all within an ethical, student-centred environment. This

model demonstrates how Islamic education can reach a global audience without

the need for physical campuses, making it cost-effective and adaptable.

Chapter 8, we explored the International Islamic Cyber University (IICU) model, a fully accredited online university. While more resource-intensive, this model holds the potential for an independently operated institution offering degrees. The recommended approach is to begin with the IICEC model, allowing time to establish partnerships, refine the platform, and build credibility before transitioning to the IICU structure,

This book

aims to be a foundational guide for educators, administrators, and policymakers

interested in establishing Cyber Education systems rooted in Islamic values. By

combining the advancements of modern technology with the ethical framework of

Maqasid al-Shariah, we aspire to create a sustainable, accessible, and

value-driven educational model that serves students worldwide

DR SHAYA’A

bin OTHMAN, ( 2024.11.08 )

SIRI ILMU UNTUK AMALAN BERSAMA BIL: 3

UNIVERSAL CRESCENT STANDARD CENTER

[UCSC]

ABSTRAK

Arak

merupakan najis dadah yang bebas disalah gunakan di dunia. Ia mengganggu otak

terutamanya pada pusat sistem saraf, mengganggu kawalan percakapan, pemikiran,

emosi dan pergerakan otot-otot. Walaupun ia diambil kadar yang sedikit, ianya

mempunyai kesan sampingan seperti, mengurangkan sensitif kepada kesakitan,

rasa, , penglihatan, ingatan, sexual,

Kerosakan jangka panjang kepada organ-organ peting termasuk, hati, jantung,

pankreas dan otak. Juga ia boleh menyebabkan sakit kanser, darah tinggi

dan kurang daya tahanan kepada penyakit. Arak telah terbukti mencacatkan bayi

dalam kandungan ibu. Bayi yang di lahir akan mengalami kecacatan seumur

hidupnya. Penyakit ketagih arak atau “alkoholisme’

menyebabkan beberapa masalah sosial: membunuh, membunuh diri, kecederaan,

kemalangan Jalan raya dan jenayah berat [violent crime]. Arak

ialah satu faktor yang menyebabkan 50% daripada jumlah kematian daripada

kecederaan. Di Amerika Syarikat sahaja membelanjakan sejumlah hamper RM700 bilion

[USD 200 billion ] setiap tahun dalam mengatasi berbagai masalah berkaitan

dengan arak. Arak membunuh seorang manusia setiap 10 saat, atau lebih dari 3.3 jutaan manusia dalam setahun (UNReport,2012) Arak

merupakan Pengganas yang mengganas untuk menghancurkan negara dan tamadun

manusia.

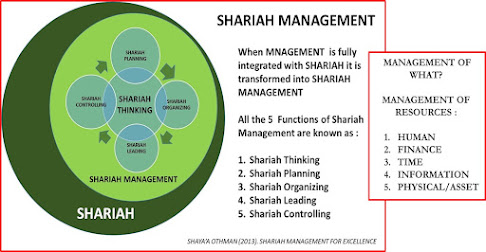

APPLICATION OF MAQASID SHARIAH AS MANAGEMENT STRATEGY OF AN ORGANIZATION

By DR. SHAYA'A OTHMAN

( Talk as Guest Speaker at Al Madinah International University, Malaysia [MEDIU] on 2023.10.30, on the occasion of Academia Month 2023 )

PLEASE CLICK BELOW TO GO OR DOWNLOAD THE SLIDE

The Summary of the Talks given by Dr SHAYA'A OTHMAN SAID is as follows;

This lecture by Dr SHAYA'A OTHMAN at Al Madinah International University, Malaysia [MEDIU] in conjunction with Malaysia Acamedic Month on 2023.10.30, Includes: 1. ISLAM is a Way of Life, Perfected, Completed, Accepted and Named by Allah [God] Himself as mentioned in The Last Testament [Quran] Chapter 5 Verse 3.

3. Maqasid Shariah [ Ultimate Objectives of Sharia ] which includes, Protection of Religion, Protection of Human Life, Protection of Human intelligence, Protection of Human Offspring and Protection of Wealth and Resources.

6. Shariah Management Strategy which should be implemented in the Strategy Process of Management resulting in the creation of a New Main Stream Islamic Economy, which humanistic than that of a Secular Conventional Economy which is less humanistic in nature.